MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

UNIVLMM - Universal LIBOR Market Model Add-in

UNIVLMM - Universal LIBOR Market Model Add-in

UNIVLMM implements the cutting edge multi-factor LIBOR Market Model and "Brace-Gatarek-Musiela" (BGM) model to price and risk manage interest rate derivatives, including multicallable amortizing and accreting Swaptions; Delivery Options in "Cheapest To Deliver" (CTD) Bond Futures; Exotic Interest Rate derivatives such as AutoFlex Caps; Knock-out caps; Reset Caps; Trigger knock-out/knock-in Swaps/inverse floaters; Spread Options; Captions; Options on swaptions; Callable Power Reverse Dual Currency (PRDC) swaps and notes; Callable range accrual dual currency quanto notes; Bermudan Callable CMS spread bonds; Callable Capped FRNs; Target Redemption Notes (TARNs) and FX Target Redemption Notes (FX- TARNs), including Reverse Floating TARNs; Crescentos / Snowballs / Ladders / Lift notes; ladder inverse floaters; Ratchets and Bermudan callable fixed to floater (flip flop), including step-up fixed rates. UNIVLMM allows you to calibrate the LIBOR Market Model's multi-factor interest rate volatility term structure based on individual CAPLET volatilities and/or market quotes for traded instruments (e.g. swaptions, caps and floors), including fitting expected correlations between different parts of the curve. Calibration and pricing are very fast.

The UNIVLMM - Universal LIBOR Market Model Add-in requires UNIVSWAP - Universal Swap Add-in.

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Click the thumbnails below for screenshots of our sample spreadsheets: |

|

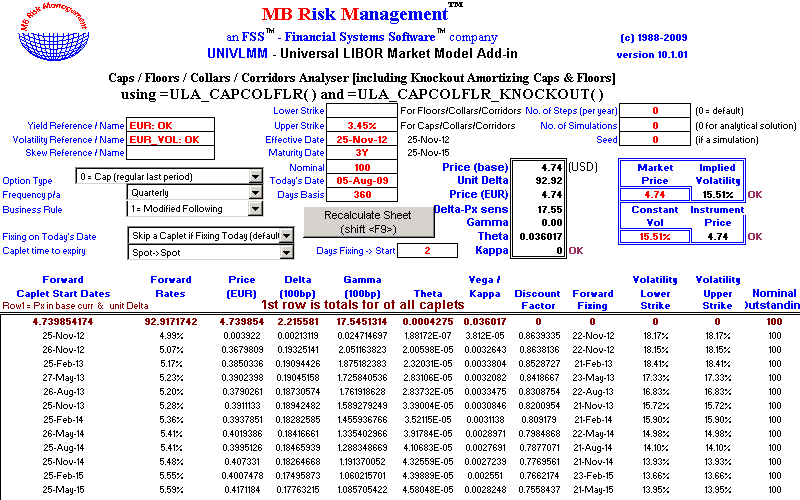

Caps / Floors / Collars / Corridors Analyser Caps / Floors / Collars / Corridors Analyser |

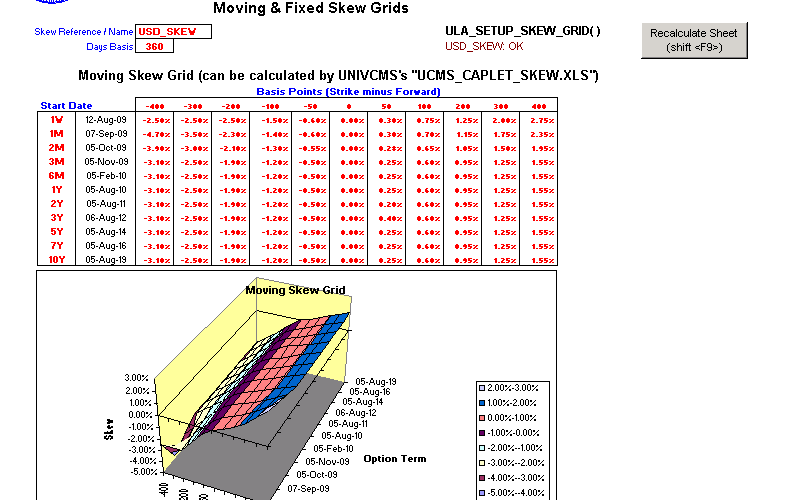

Moving & Fixed Skew Grids Moving & Fixed Skew Grids |

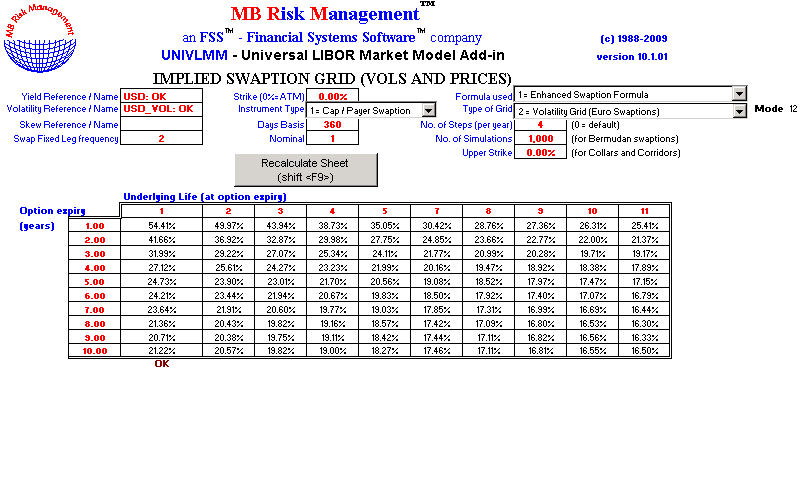

Implied Swaption Grid (Vols And Prices) Implied Swaption Grid (Vols And Prices) |

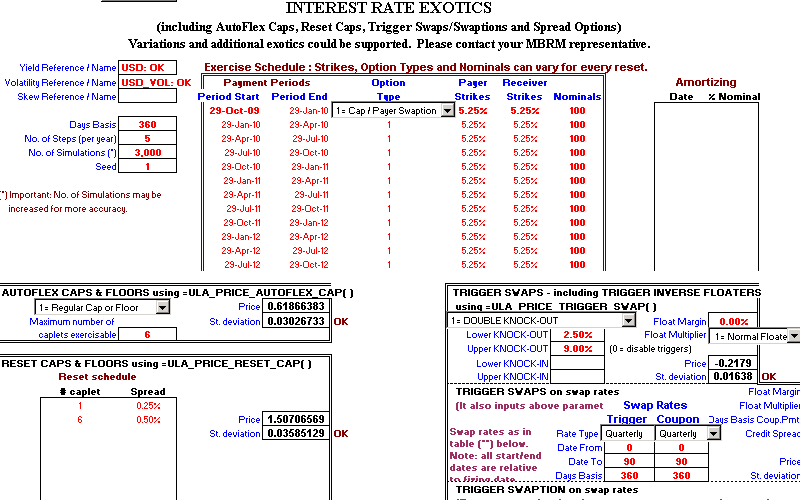

Interest Rate Exotics Interest Rate Exotics |

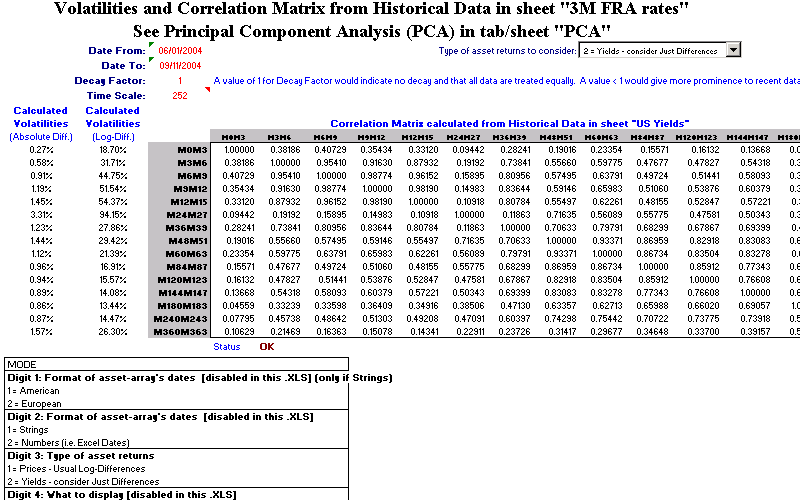

Volatilities And Correlation Matrix From Historical Data Volatilities And Correlation Matrix From Historical Data |

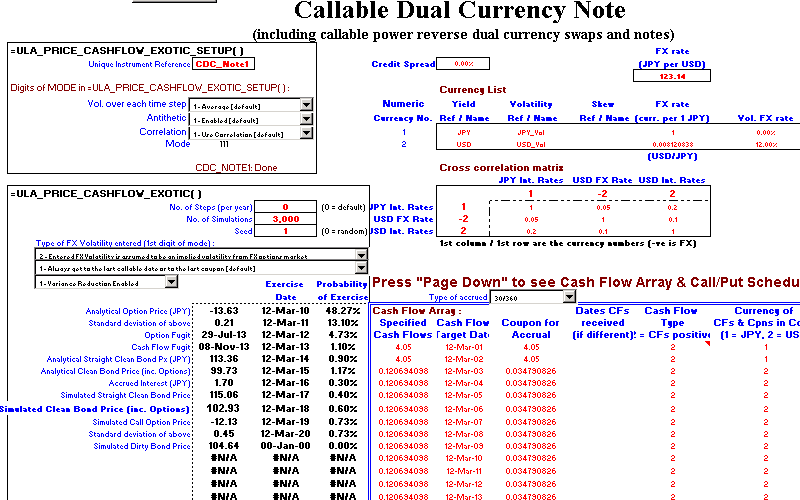

Callable Dual Currency Note Callable Dual Currency Note |

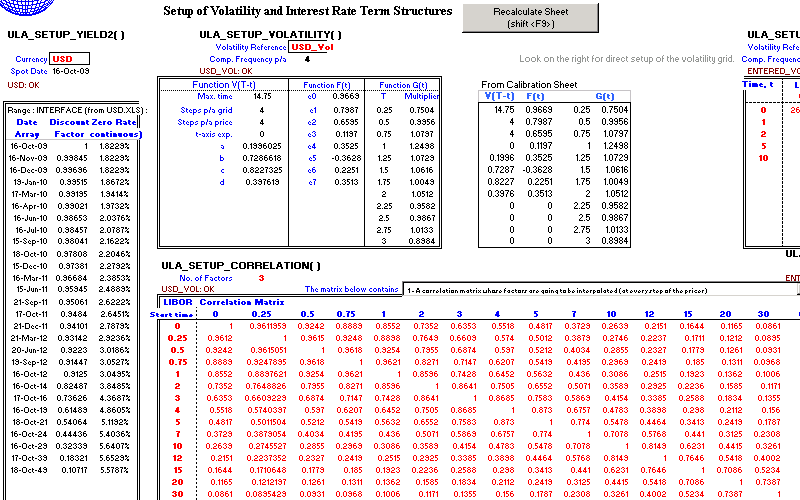

Setup Of Volatility And Interest Rate Term Structures Setup Of Volatility And Interest Rate Term Structures |

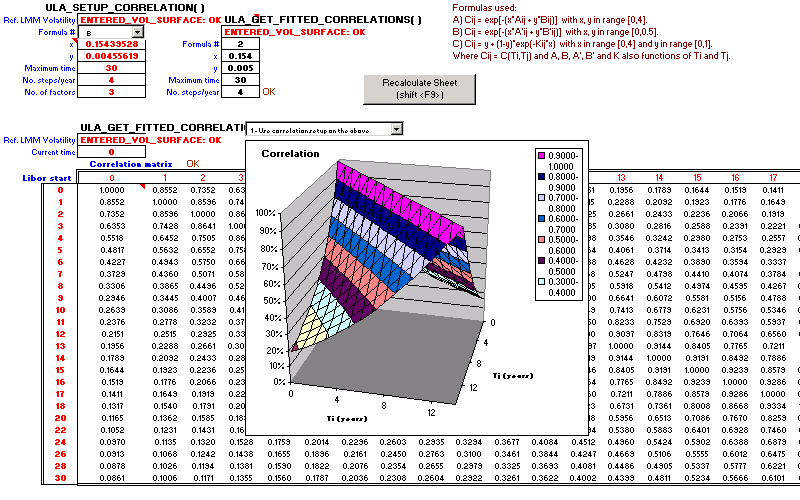

Setup/Display Of Correlation Surface Setup/Display Of Correlation Surface |