MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

UNIVOPT - Universal Options Add-in

UNIVOPT - Universal Options Add-in

UNIVOPT is regarded by many dealers and risk managers as the industry standard option pricing and risk management system. Amongst the new features are 6 new models. The options add-in calculates option prices and implied volatilities using the Black, Black-Scholes, Garman- Kolhagen, Cox-Rubinstein (binomial) models, as well as proprietary models for normally distributed underlying instruments. UNIVOPT handles European and American style options on bonds, commodities, currencies, futures (including 3M interest rate futures) and shares (including constant dividend streams and discrete dividend payments). It also calculates sensitivities, such as delta, gamma, fugit, kappa (vega), rho, theta and theta2. UNIVOPT also contains a warrant pricing function which takes into account dilution (which is very useful when analysing warrants about to be issued by companies on their own stock).

UNIVOPT enables the production of pricing matrices, risk return profiles and implied volatility analysis for either individual options or portfolios.

A number of example spreadsheets are supplied free with UNIVOPT, which enable the user to price and risk manage option portfolios "straight out of the box" without any programming or "spreadsheet" work.

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Click the thumbnails below for screenshots of our sample spreadsheets: |

|

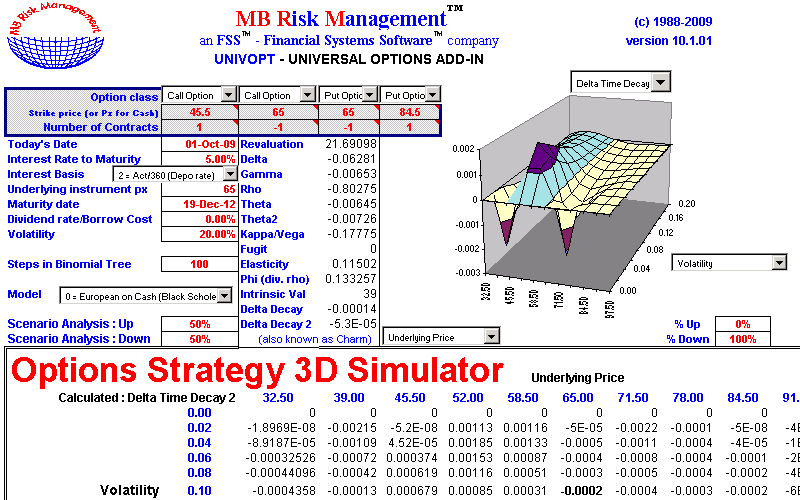

Options Strategy 3D Simulator Options Strategy 3D Simulator |

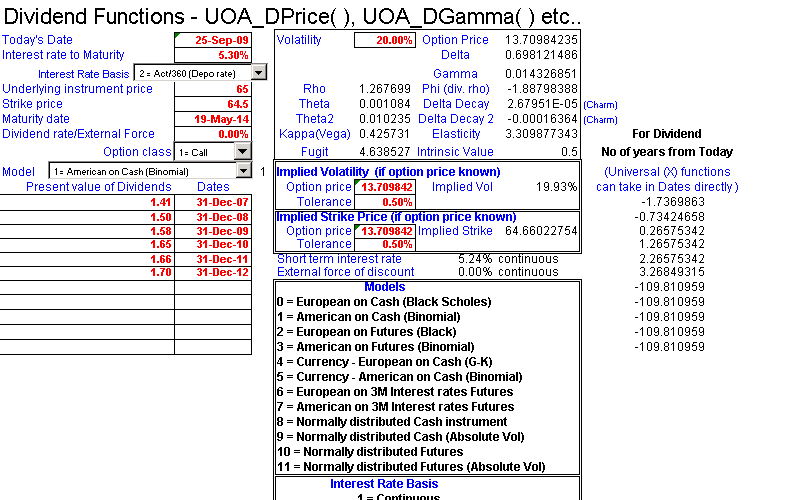

Dividend Functions Dividend Functions |

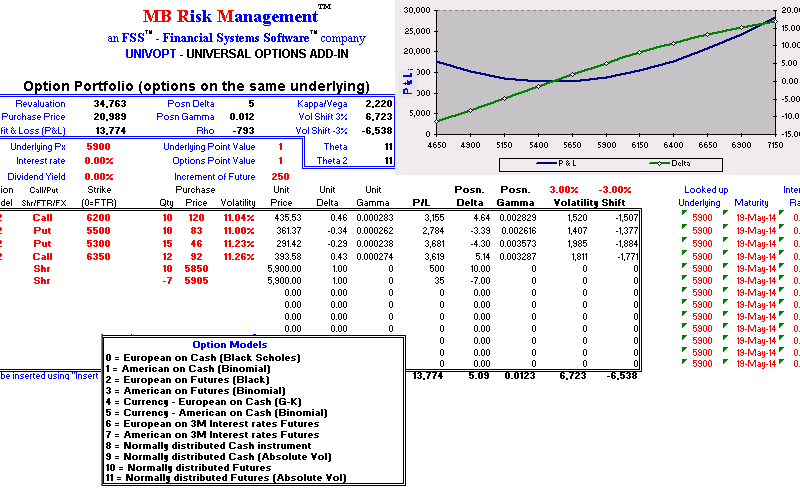

Option Portfolio Option Portfolio |

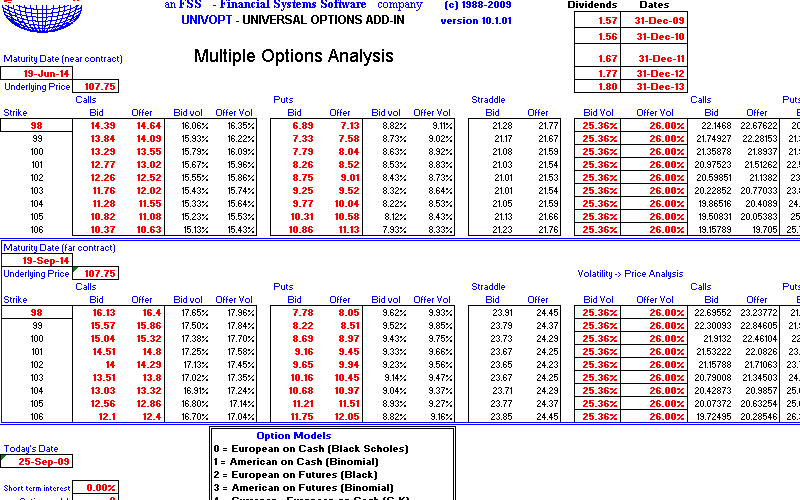

Multiple Options Analysis Multiple Options Analysis |

Warrant Hedge Analyser Warrant Hedge Analyser |

|