MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

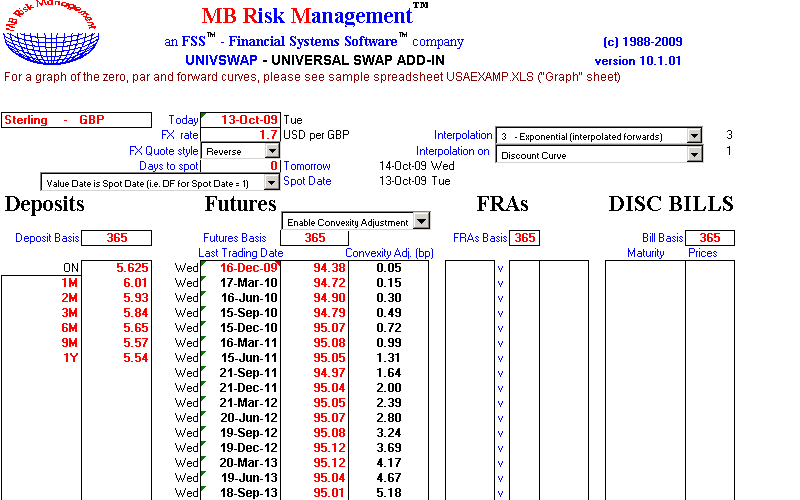

UNIVSWAP - Universal Swap Add-in

UNIVSWAP - Universal Swap Add-in

The swap add-in is an interest rate and cross-currency swap add-in. The add-in builds a No-Arbitrage term structure model for interest rates and volatilities (using mean reversion) from any combination of bonds, swaps, bills, deposits and/or futures. This term structure is used to consistently price instruments, including Bonds, Swaps, FRAs, IRGs, Caps, Collars, Floors, Corridors, Digitals. The approach used for volatility modelling is based on the extended Vasicek (Hull-White) models, with a number of proprietary improvements. This gives maximum flexibility to quantify both standard and non-standard transactions. The swap add-in enables the user to check the prices being quoted by the counterparty, increasing the user's competitive advantage. Multi-currency portfolios are continuously marked to market - improving P&L and Risk monitoring.

UNIVSWAP - Universal Swap Add-in incorporates, at no extra charge, full copies of the following four Universal Add-ins :

| UNIVOPT - Universal Options Add-in | |

| UNIVEXOT - Universal Exotics Add-in | |

| UNIVYLD - Universal Yield Add-in | |

| UNIVINT - Universal Interpolating Add-in |

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Graph of Zero, Par and Forward Curves

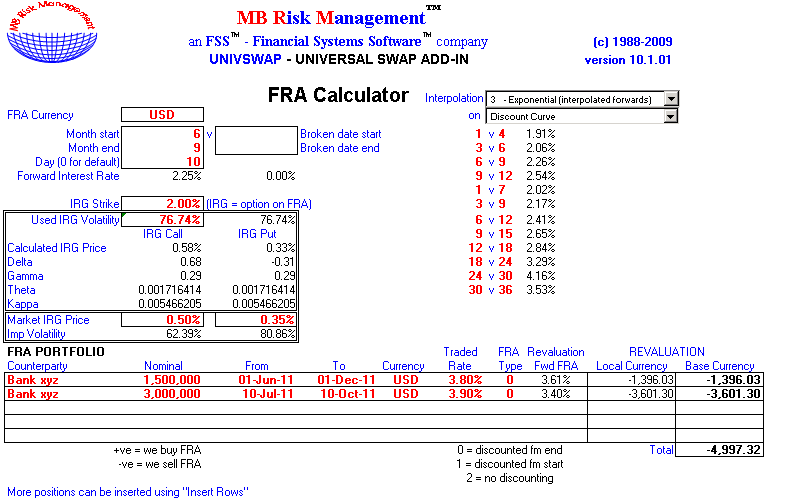

Graph of Zero, Par and Forward Curves FRA Calculator

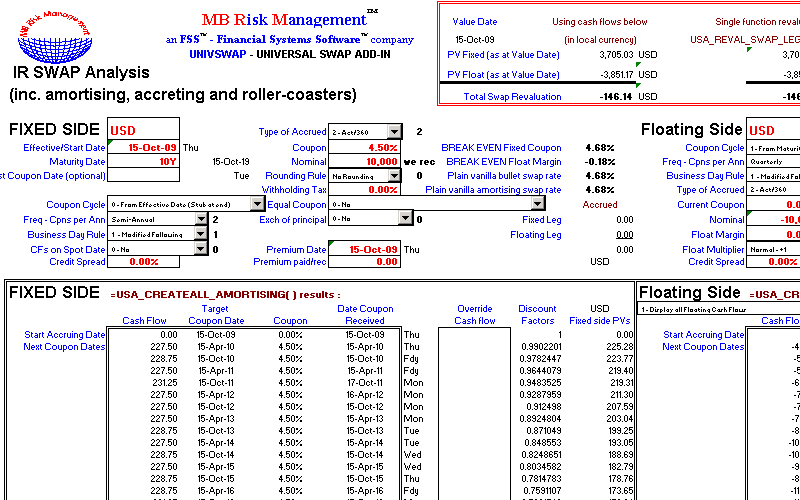

FRA Calculator Swap Analysis

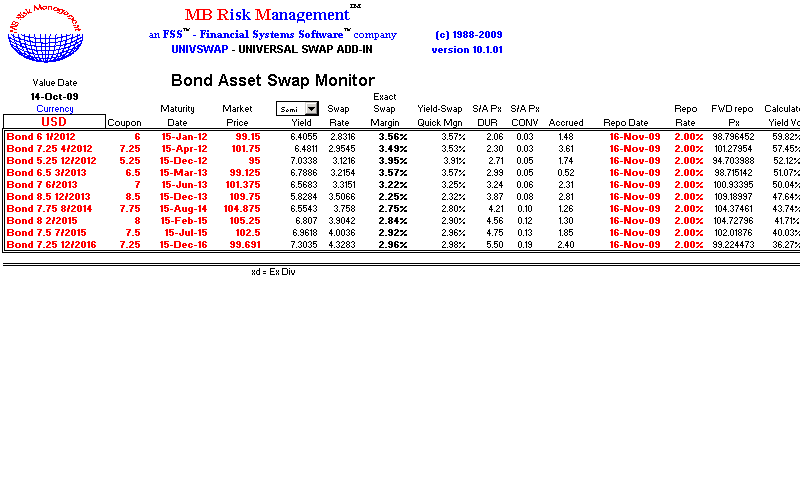

Swap Analysis Bond Asset Swap Monitor

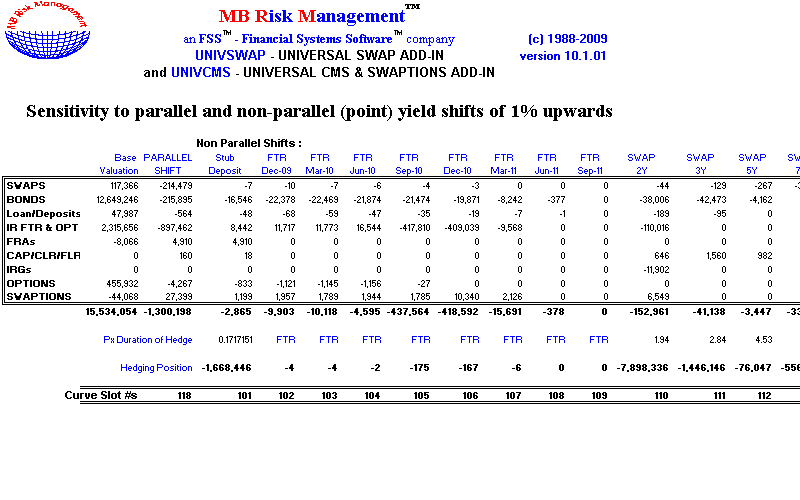

Bond Asset Swap Monitor Portfolio IR Sensitivity Analysis (Portfolio)

Portfolio IR Sensitivity Analysis (Portfolio) Portfolio IR Sensitivity Analysis (Analysis)

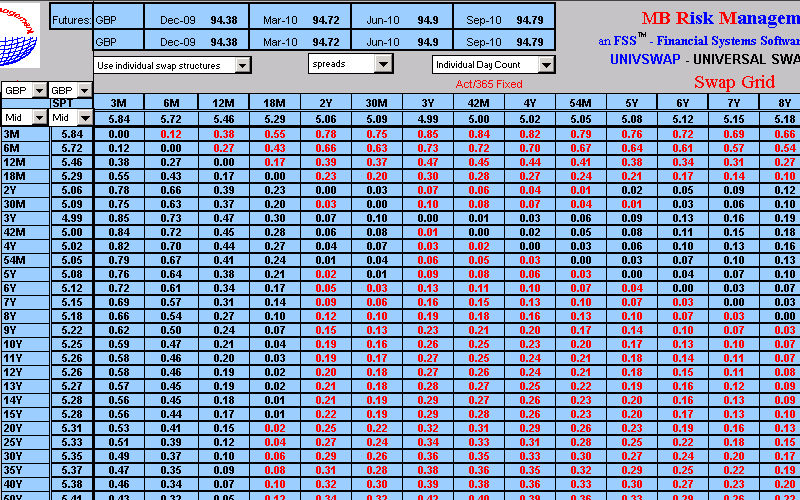

Portfolio IR Sensitivity Analysis (Analysis) 'Matrix' tab of SwapGrid.xls

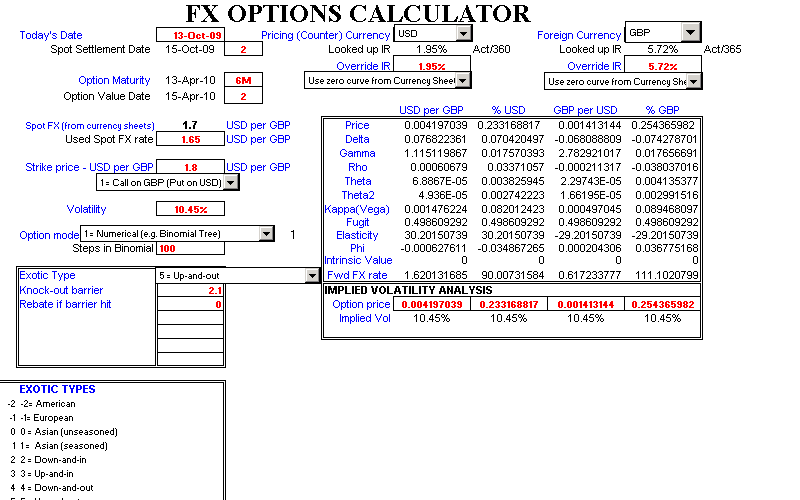

'Matrix' tab of SwapGrid.xls FX Options Calculator

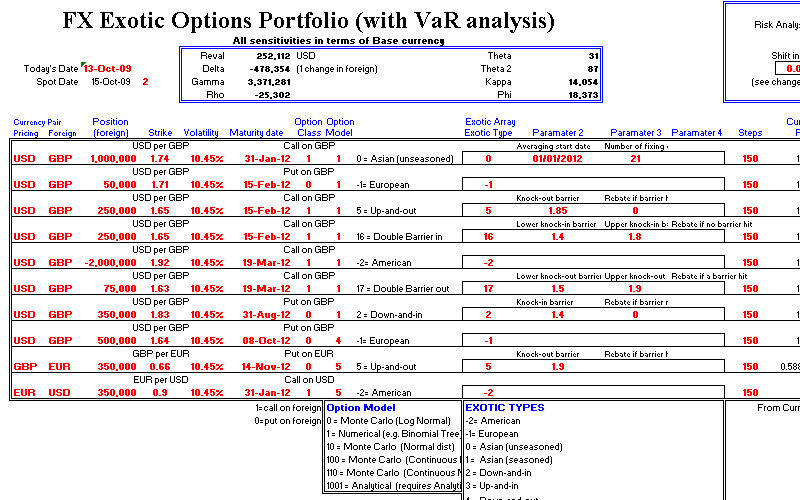

FX Options Calculator FX Exotic Options Portfolio (with VaR analysis)

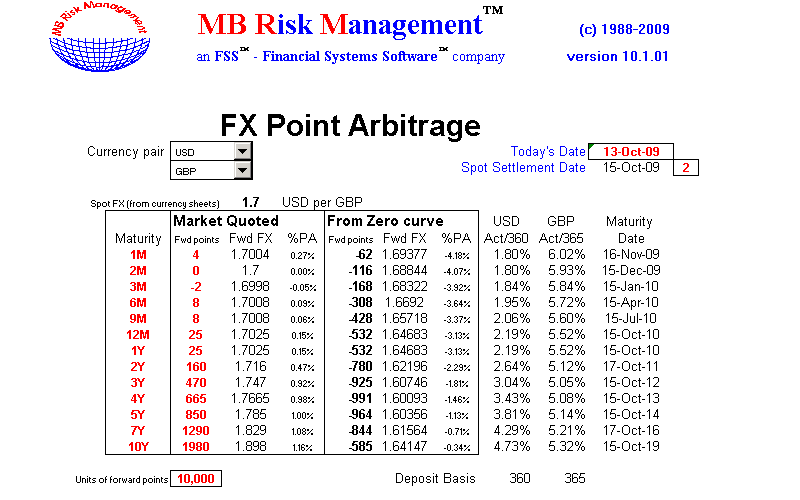

FX Exotic Options Portfolio (with VaR analysis) FX Point Arbitrage

FX Point Arbitrage 'Cash' tab of Currency Sheet

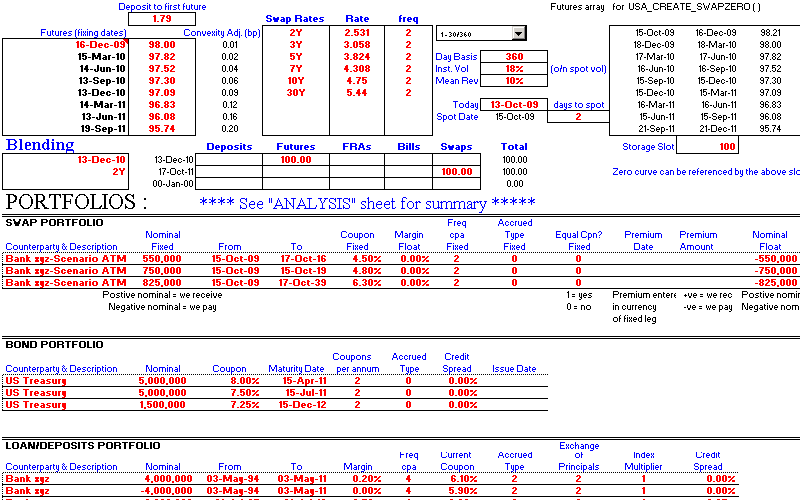

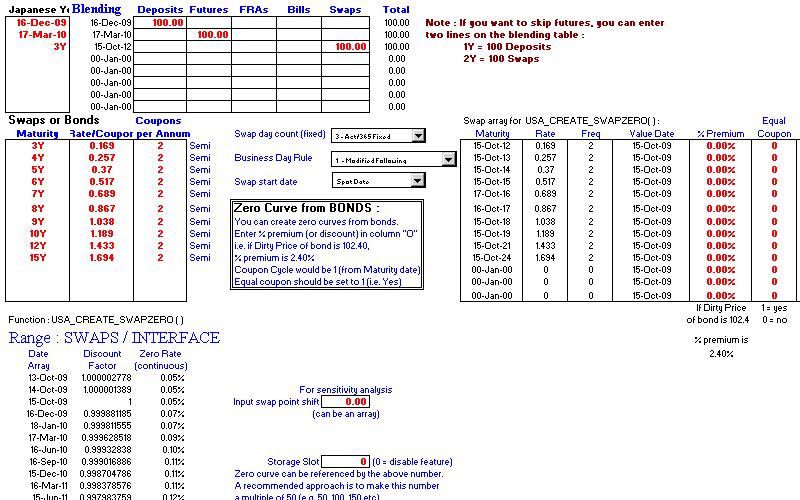

'Cash' tab of Currency Sheet Swaps-Bonds-Blending

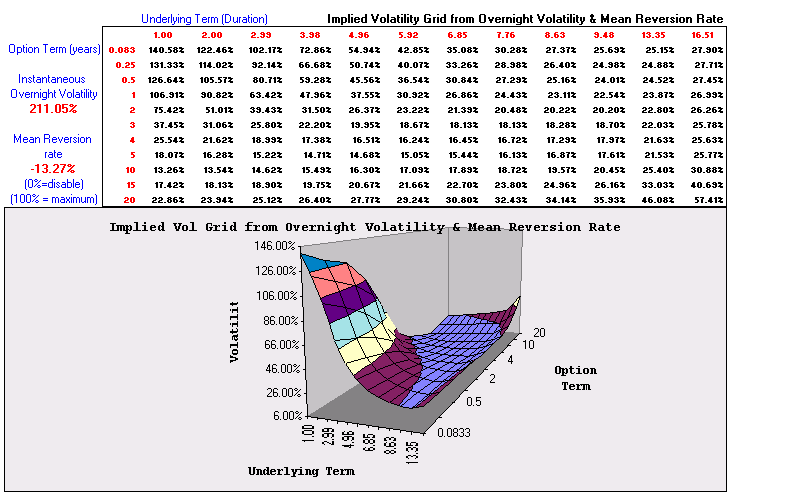

Swaps-Bonds-Blending 'Volatility' tab of Currency Sheet

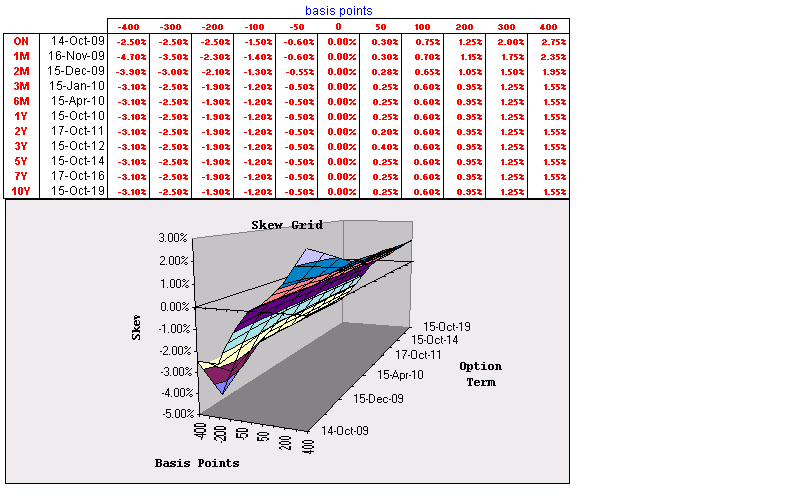

'Volatility' tab of Currency Sheet 'Volatility Skew' tab of Currency Sheet

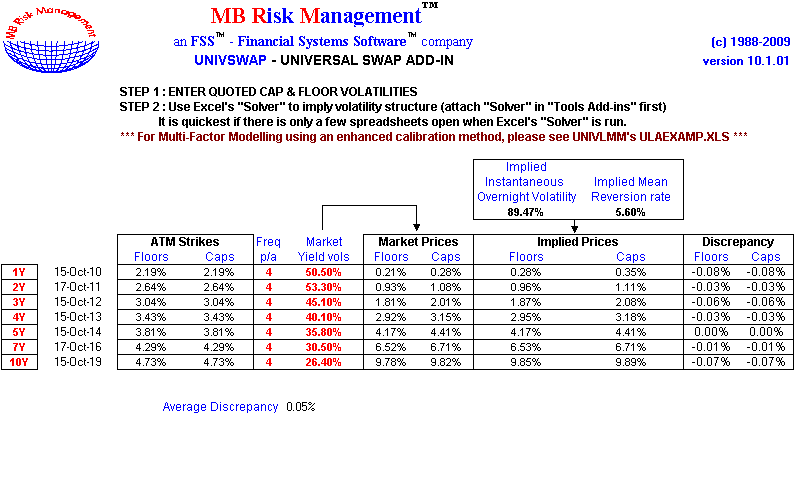

'Volatility Skew' tab of Currency Sheet 'Vol Calibration 1' tab of Currency Sheet

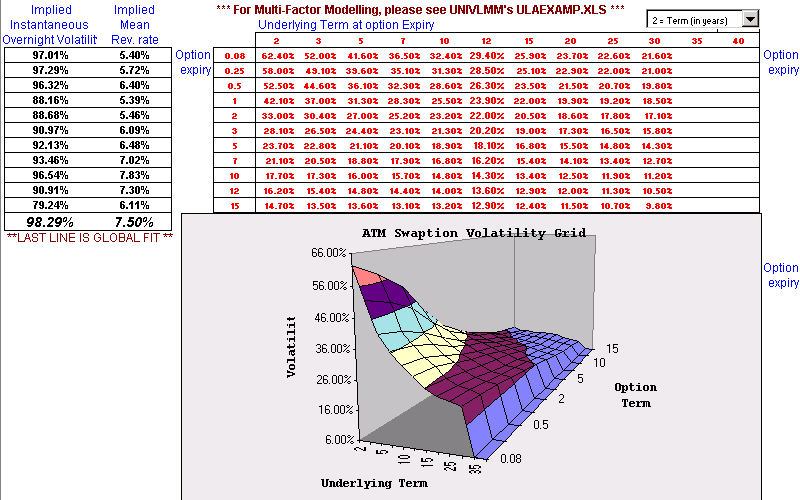

'Vol Calibration 1' tab of Currency Sheet 'Vol Calibration 2' tab of Currency Sheet

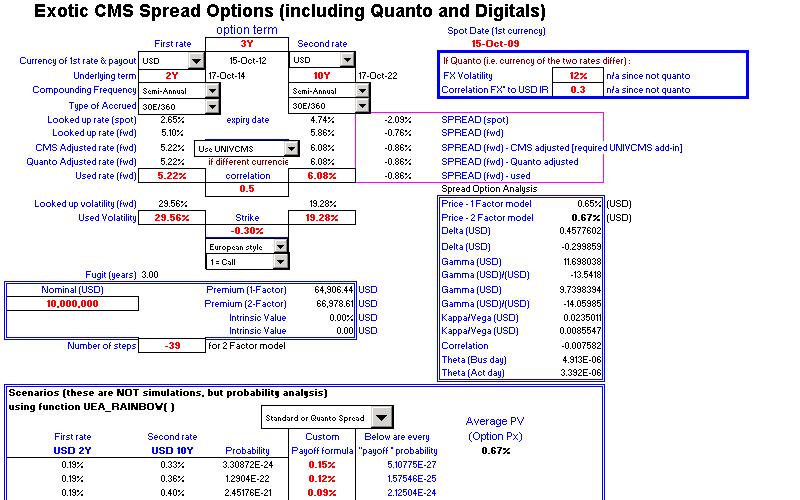

'Vol Calibration 2' tab of Currency Sheet Exotic CMS Spread Options (including Quanto and Digitals)

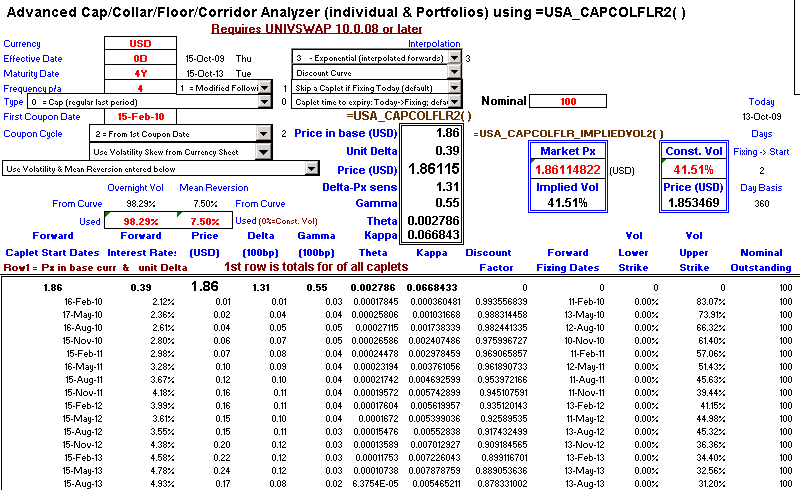

Exotic CMS Spread Options (including Quanto and Digitals) Advanced Cap/Collar/Floor/Corridor Analyzer

Advanced Cap/Collar/Floor/Corridor Analyzer