MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

UNIVCRD - Universal Credit Risk Add-in

UNIVCRD - Universal Credit Risk Add-in

UNIVCRD calculates a portfolio's exposure to counterparty risk. A major feature is the use of an analytical methodology which provides a considerable speed advantage over traditional Monte Carlo approaches and which supports default correlations. Instantaneous calculation of credit risk enables real-time monitoring by traders and risk managers.

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Click the thumbnails below for screenshots of our sample spreadsheets: |

|

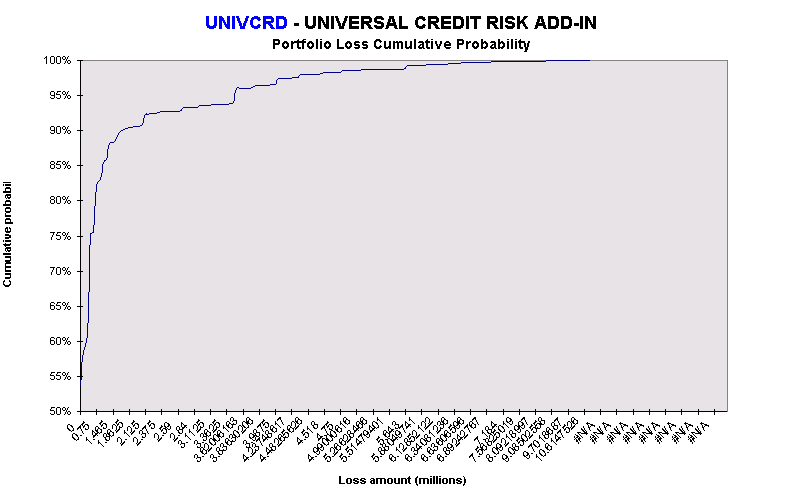

Portfolio Loss Cumulative Probability Portfolio Loss Cumulative Probability |

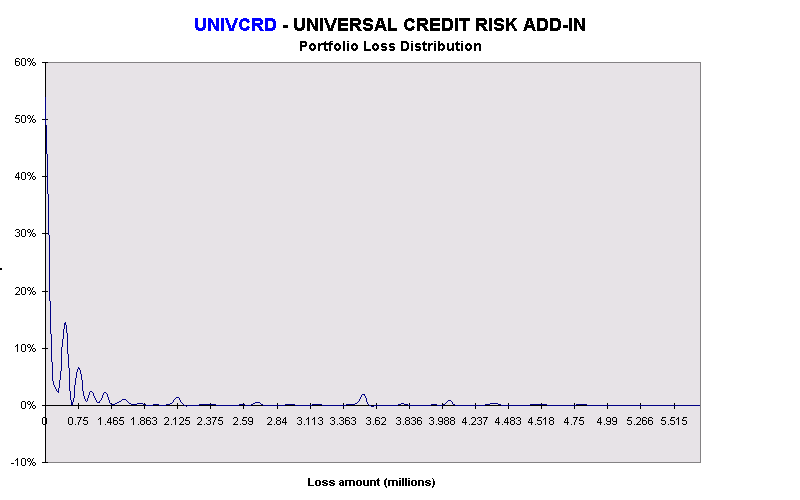

Portfolio Loss Distribution Portfolio Loss Distribution |

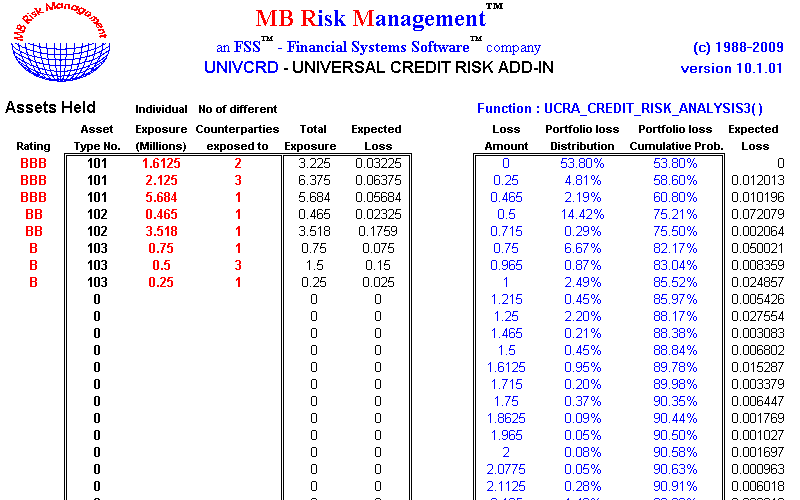

Function : UCRA_CREDIT_RISK_ANALYSIS3( ) Function : UCRA_CREDIT_RISK_ANALYSIS3( ) |

|