MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

UNIVCMS - Universal CMS & Swaptions Add-in

UNIVCMS - Universal CMS & Swaptions Add-in

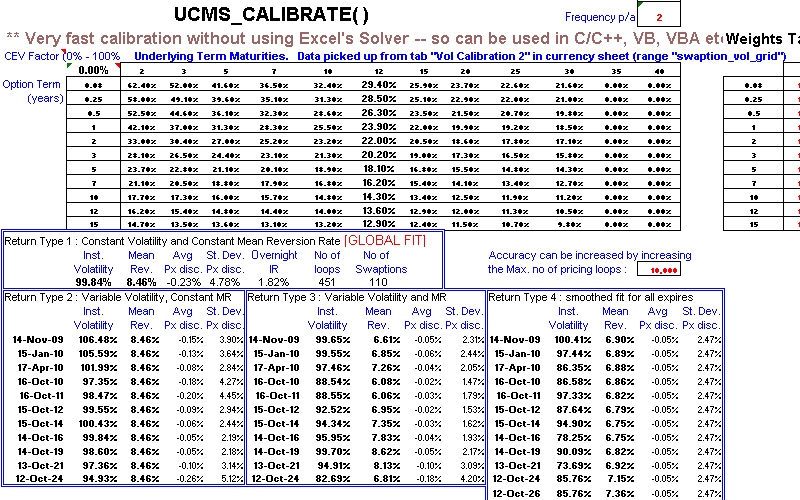

This is an optional add-in for users of our Universal Swap Add-in who require the pricing and risk management of Constant Maturity Swaps (CMS) and/or European, Bermudan and American style options on Bonds or Swaptions. Analyses multi-callable amortizing swaps and bonds, including passing in a Constant Elasticity of Variance (CEV) and full Swaption Volatility grid directly to BDT/BK pricing model. Also handles CMS Quanto Caps, Collars, Floors and Corridors. The approach used is based on the Black-Derman-Toy (BDT) and/or extended Vasicek (Hull-White) interest rate models for implementation of a No-Arbitrage term structure model for interest rates (with mean reversion), and utilises a balanced trinomial tree for increased accuracy. Market standard calculation of swaption prices AND SENSITIVITIES assuming constant "black" volatility are also implemented using a single function call. UNIVCMS also implements a very fast calibration of extended Vasicek (Hull-White) volatility and Mean Reversion term structures without using Excel's Solver.

The UNIVCMS - Universal CMS & Swaptions Add-in requires UNIVSWAP - Universal Swap Add-in.

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Click the thumbnails below for screenshots of our sample spreadsheets: |

|

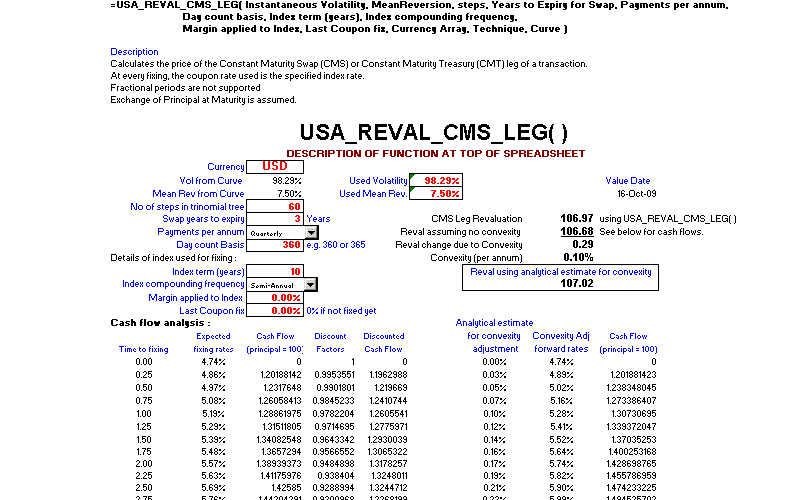

Constant Maturity Swap (CMS) or Constant Maturity Treasury (CMT) Constant Maturity Swap (CMS) or Constant Maturity Treasury (CMT) |

Very Fast Calibration Without Using Excel's Solver Very Fast Calibration Without Using Excel's Solver |

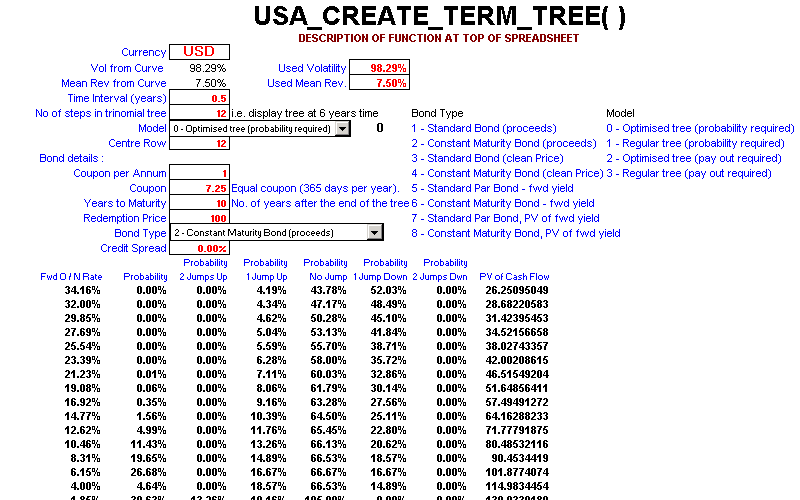

Create Trinomial Tree Create Trinomial Tree |

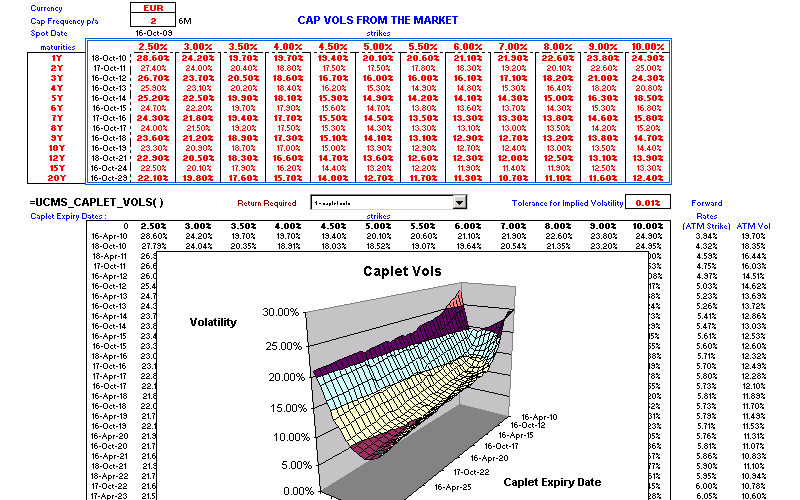

Implying The Caplet Vols From CAP Vols Implying The Caplet Vols From CAP Vols |