MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

UNIVEXOT - Universal Exotics Add-in

UNIVEXOT - Universal Exotics Add-in

The exotics add-in calculates prices, sensitivities and implied volatilities of Exotic options, including Average price (Asian), Barrier and double Barrier (Knock-out and Knock-ins), Quanto Basket Asian options, Digital, Compound, Contingent, Ladder, Lookback and one and two Touch options on bonds, commodities, currencies, futures and shares (including constant dividend streams and discrete dividend payments). Windows Barriers also supported (windows can be up front, in middle or at end). For maximum flexibility and sensitivity testing, it allows the user to choose to either a numerical (e.g. binomial tree) algorithm or a flexible Monte Carlo simulation algorithm. Smoother handling of barriers are implemented to improve accuracy of numerical models.

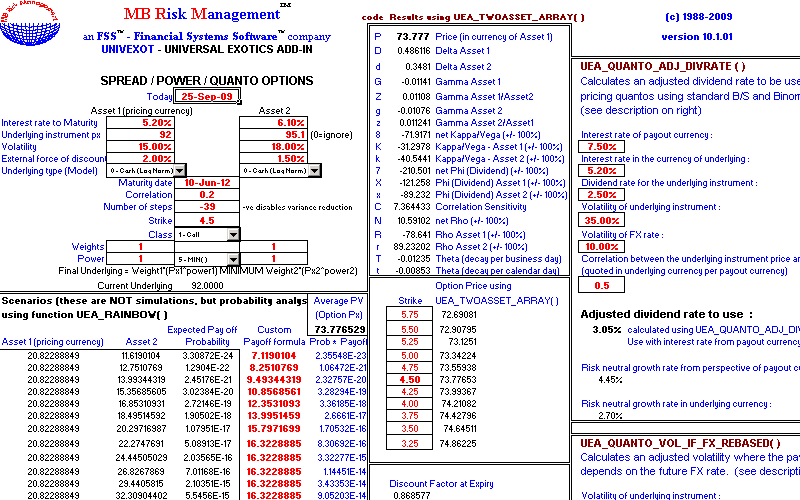

With a single function call, UNIVEXOT calculates the full sensitivities of Spread and Power options. UNIVEXOT also analyses two asset Rainbow options where any user specified pay off formula can be entered. When UNIVEXOT is combined with UNIVOPT, you have a formidable combination for most standard and exotic options in an easy to use package.

A number of example spreadsheets are supplied free with UNIVOPT, which enable the user to price and risk manage option portfolios "straight out of the box" without any programming or "spreadsheet" work.

The Universal Exotics Add-in requires UNIVOPT - Universal Options Add-in

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Click the thumbnails below for screenshots of our sample spreadsheets: |

|

UEA XARRAY Functions UEA XARRAY Functions |

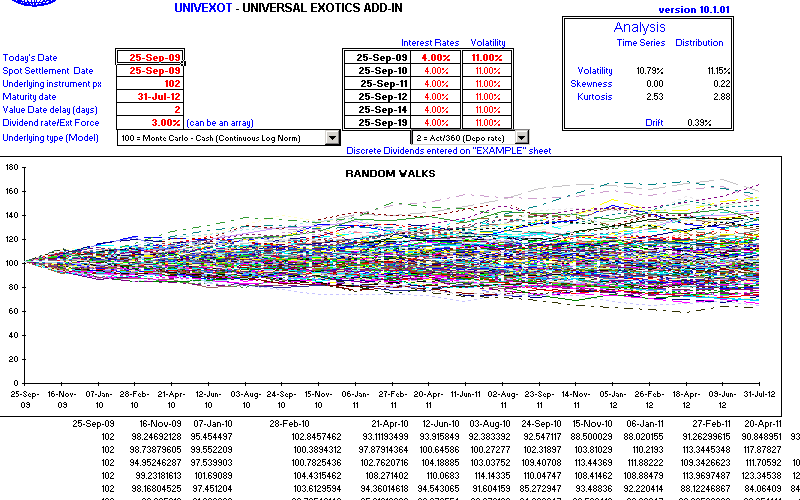

Random Walk Random Walk |

Spread / Power / Quanto Options Spread / Power / Quanto Options |

Hybrid Combined Average Strike and Average Price Options Hybrid Combined Average Strike and Average Price Options |

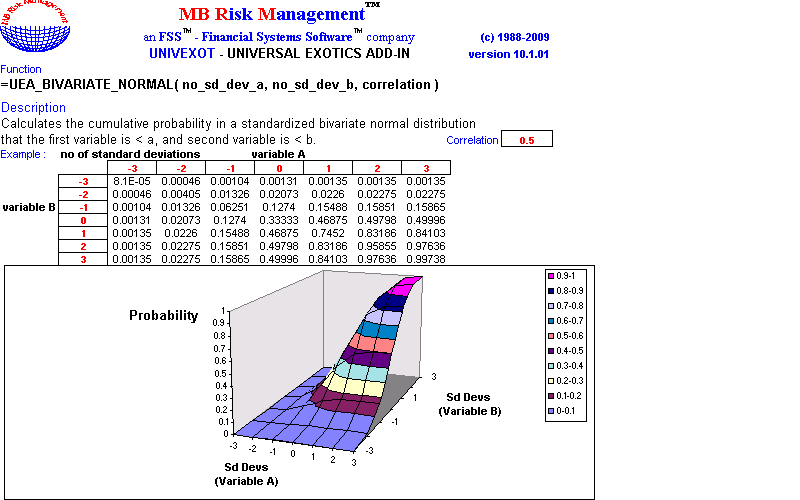

Bivariate Bivariate |

Vols, IR & FX Correlations Vols, IR & FX Correlations |

Quanto Basket Analyser Quanto Basket Analyser |

|