MBRM - MB Risk Management

29 Throgmorton Street

London EC2N 2AT

United Kingdom

| Switchboard: | +44 20-7628 2007 |

| Support: | +44 20-7628 2008 |

sales@mbrm.com

MBRM Technical Support Facilities

UNIVFDIF - Universal Finite Difference Add-in

UNIVFDIF - Universal Finite Difference Add-in

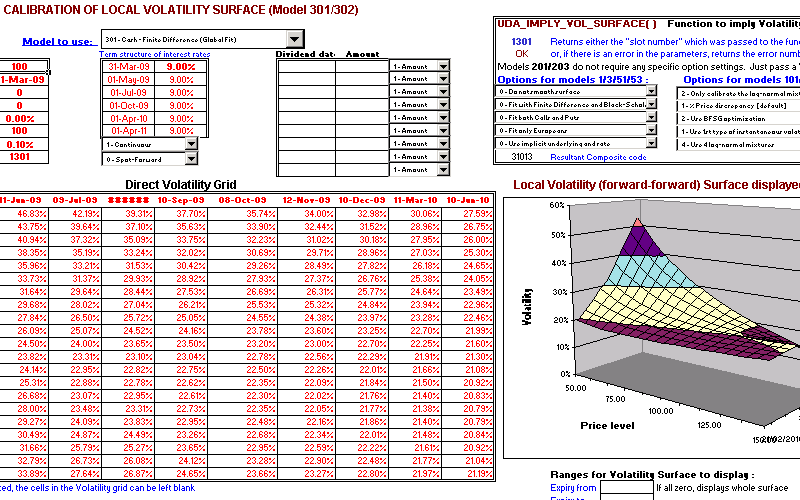

UNIVFDIF implies the local volatility surface and then prices and calculates the full sensitivities of European, American style and Bermudan variable strike Exotic options (including discrete windowed and double barriers) on bonds, commodities, currencies, futures and shares (including discrete dividend payments). The add-in uses the finite difference algorithm which is more advanced than standard binomial trees. Full term structure of interest rates and Multi-Dimensional Local Volatility Surface are handled.

Cost Saving Bundle

| UNIVDRV - Universal Derivatives Add-in is an inclusive package of : | |

| UNIVEXOT+ - Universal Analytical Exotics Add-in | |

| UNIVFDIF - Universal Finite Difference Add-in | |

| UNIVGARCH - Universal Garch Add-in | |

Why not consider MBRM Comprehensive Combined Package : An inclusive package of our main software packages (This would be a massive saving on the individual selling price of these packages)

CLICK HERE to see our latest Price List.

Click the thumbnails below for screenshots of our sample spreadsheets: |

|

Calibration Of Local Volatility Surface Calibration Of Local Volatility Surface |

|